Filipinos often seek loans to address various financial needs, from covering unexpected expenses to funding business ventures. Loan apps offer convenience, speed, and accessibility. With minimal requirements and swift approval processes, these apps provide a lifeline for individuals lacking access to bank loans or facing urgent financial constraints.

Moreover, Filipinos appreciate the transparency and flexibility offered by loan apps, allowing them to manage repayments efficiently. In a country where financial inclusion remains challenging, these digital platforms empower Filipinos to navigate financial hurdles easily.

This blog post will guide you to 5 legit online loan apps you can use in the Philippines.

Top 5 Legit Online Loan Apps in the Philippines

Tala

Tala started offering digital loans to Filipinos in 2017. They operate in three countries: the Philippines, Kenya, and Mexico.

Loan Amount: The first loan is limited to PHP 1,000 to PHP 15,000. The succeeding loan amount increases depending on your record.

Interest Rate: Starts at 0.5% daily

When borrowing from Tala, you’ll encounter these fees:

- A one-time processing fee of 3.99% of the borrowed amount.

- Daily service fees range from 0.43% to 0.5% on top of the borrowed amount, accumulating until either 61 days elapse or full repayment is made, whichever comes first.

Requirements

- Android phones running OS 4 or higher.

- Valid government-issued ID

Cashout Options

- Bank account

- Padala center

- Coins.ph

Cashalo

Cashalo, a mobile-centric lending platform, collaborates with JG Summit’s subsidiary Express Holdings Inc. and Oriente. Extending loans to underserved population segments aims to enhance financial inclusion in the Philippines.

Loan Amount: PHP 1,000 to a maximum of PHP 7,000

Interest Rate: 0.10% daily interest rate

Loan Term: Payment terms can extend up to 90 days.

When borrowing from Cashalo, you’ll encounter these fees:

- One-time processing fee of 10%

- Additional interest charges if you fail to meet payment due dates, which are calculated separately based on the principal amount borrowed.

Requirements

- Valid government-issued ID

- Proof of billing

- Valid work ID

- Recent payslip

- Bank account details

Cashout Options

- Bank account

- GCash

- PayMaya

GLoan

GLoan is a personal loan service available through the GCash app, perfect for times when you’re short on cash. Once approved, the loan amount is added to your e-wallet within 24 hours.

Loan Amount: PHP 1,000 to a maximum of PHP 125,000

Interest Rate: 0.053% – 0.233% daily interest depending on your eligibility and chosen payment term

Loan Term: 5, 6, 9, 12, 15, 18, and 24 months

When borrowing from GLoan, you’ll encounter these fees:

- A one-time deduction of 3% from your total loan amount.

- Late Payment Fee: 1% of your loan amount for each missed due date, plus an additional 0.15% of the outstanding balance multiplied by the number of days past the due date.

Requirements

- 21-65 years old

- Filipino citizen

- Fully verified GCash user

- Have a good credit record and have no history of fraudulent transactions

Cashout Options

- GCash MasterCard

- Official GCash partner locations

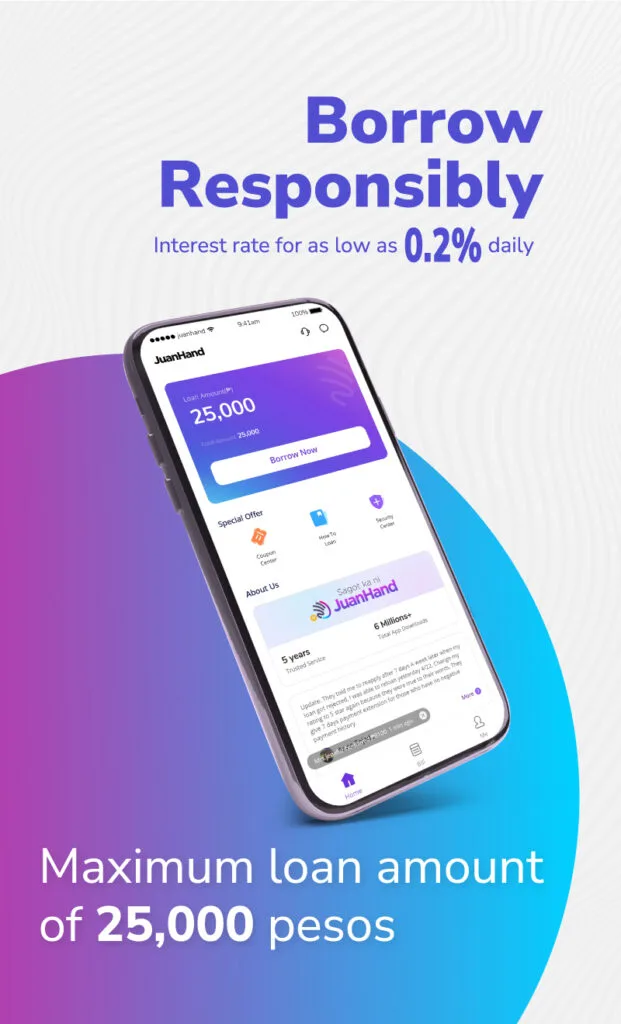

JuanHand

JuanHand is one of the leading fintech platforms in the Philippines. It provides quick, seamless, and affordable financial access to the creditworthy yet underserved. The platform is safe and secure to use, ensuring all client information is protected and encrypted in full compliance with NPC regulations.

Loan Amount: PHP 2,000 to a maximum of PHP 25,000

Interest Rate: Starts at 0.49% daily

Loan Term: The shortest duration for payment is 90 days, while the longest is 180 days.

When borrowing from JuanHand, you don’t have to pay any transaction fee.

Requirements

- A Filipino citizen

- 20-60 years old

- Have a stable source of income

- Can present at least one government-issued ID

Cashout Options

- E-wallet

- Over-the-counter withdrawal

UNO Digital Bank

UNO Digital Bank is the first full-service digital bank in Southeast Asia. It’s licensed by the Bangko Sentral ng Pilipinas and offers a new, easy, improved, and accessible way of banking.

Loan Amount: PHP 10,000 to a maximum of PHP 500,000

Interest Rate: Starts at 0.6% daily

Loan Term: The shortest payment duration is 180 days, while the longest is 1095 days (3 months).

When borrowing from UNO Digital Bank, you’ll encounter these fees:

- Processing Fee: 3% of the loan amount or PHP 500, whichever is greater, deducted from the loan proceeds.

- Late Payment Fee: 5% of the unpaid installment or PHP 500, whichever is greater.

- Loan Pre-termination Processing Fee: 3% of the unbilled amount or PHP 300, whichever is greater. This fee applies to loans exceeding 30 days; and none for under 30 days.

Requirements

- 21 and 65 years old upon loan maturity

- A Filipino citizen

- Work at or resident of Metro Manila, Cebu, Rizal, Cavite, Laguna, Pampanga, Bulacan, Batangas, Iloilo, or Davao Del Sur.

- A minimum gross monthly income of PHP 20,000

- For employed applicants: At least six months of tenure with their current employer

- For self-employed applicants: Must have operated their business for at least two years.

Cashout Options

Benefits of Online Loans

Convenience

Online loans allow you to apply from anywhere as long as you have internet access, which saves you time and effort compared to processing paperwork in a traditional bank.

Accessibility

Online loans provide access to funds for individuals who may not qualify for traditional loans due to bad credit history. Also, unlike brick-and-mortar banks, online lenders operate 24/7, allowing borrowers to apply for loans and access customer support anytime.

Speedy Approval

Online loan applications are processed quickly, often providing approval within hours or minutes.

Flexibility

Online loans come in various types, including personal loans, payday loans, and installment loans, offering flexibility to cater to different financial needs and situations.

Drawbacks of Borrowing Money Through Loan Apps

High Interest Rates

Many loan apps charge exorbitant interest rates, leading to significant long-term financial burdens for borrowers, especially those with limited repayment capacity.

Hidden Fees

Some loan apps may hide fees within the fine print, resulting in unexpected charges that increase the overall cost of borrowing and catch borrowers off guard. Additionally, many loan apps operate in regulatory gray areas, evading consumer protection laws and oversight, leaving borrowers with limited recourse in case of unfair practices or disputes.

Security Risks

Sharing personal and financial information with loan apps can expose borrowers to cybersecurity threats, including data breaches and identity theft, compromising their privacy and economic security.

Debt Traps

The accessibility and ease of borrowing through loan apps can lead to impulsive decisions and overborrowing, pushing borrowers into debt cycles from which it’s challenging to escape.

Negative Impact on Credit Score

Defaulting on loan apps can severely damage your credit score. Lenders report missed payments to credit bureaus, leading to a lower credit rating. This negatively impacts your ability to secure future loans if you often miss payments, as lenders view you as a high-risk borrower.

Additionally, poor credit scores can affect other aspects of your financial life, such as being denied rental housing, facing higher interest rates on future loans, or even difficulty securing certain jobs requiring credit checks.

Aggressive Collections

Some loan apps employ aggressive collection tactics, including harassment and threats, to recover outstanding debts, causing stress and anxiety for borrowers already struggling with repayment.

Tips on Choosing Legit Online Loans

Research thoroughly

Before committing to any online loan, research different lenders. Look for well-established companies with positive reviews and ratings from previous borrowers.

Verify credentials

Ensure that the lender is legitimate by checking whether it is licensed and regulated by relevant financial authorities in your region.

Transparent terms

Carefully read and understand all terms and conditions associated with the loan. Pay close attention to interest rates, fees, and repayment options.

Secure website

Protect your personal and financial information by choosing lenders with secure websites. Look for indicators like SSL encryption that protect your data from unauthorized access or cyber threats.

Avoid upfront fees

Be wary of lenders who request upfront payments or fees before processing your loan application. Legitimate lenders typically deduct costs from the loan amount or include them in the repayment structure.

Final Thoughts

These 5 legit online loan apps in the Philippines—Tala, Cashalo, GLoan, JuanHand, and UNO Digital Bank—offer Filipinos a convenient and accessible way to manage their financial needs.

Each app provides unique benefits, such as quick processing times, transparent terms, and minimal paperwork, making it a viable option for those who need immediate financial assistance.

However, it’s crucial to remain cautious and informed. Always verify the lender’s credentials, thoroughly understand the terms, ensure website security, and avoid any lender demanding upfront fees. Following these, you can make informed decisions and select the best online loan option to suit your financial situation.

You might want to invest wit